S-Corp

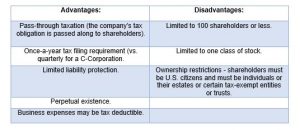

The S-Corporation (S-Corp) is a popular choice among small business owners. This type of entity allows one level of taxation, whereas C-Corporations are subject to double taxation. An S-Corp gives the advantage of pass-through taxation. This allows each shareholder to report their share of the company’s profit or loss on their individual tax returns. Liability protection is the same for an S-Corp as it would be for a C-Corp.

The S-Corporation (S-Corp) is a popular choice among small business owners. This type of entity allows one level of taxation, whereas C-Corporations are subject to double taxation. An S-Corp gives the advantage of pass-through taxation. This allows each shareholder to report their share of the company’s profit or loss on their individual tax returns. Liability protection is the same for an S-Corp as it would be for a C-Corp.

An S-Corp has ownership restrictions. All shareholders must be U.S. citizens. The company must also be a domestic corporation and must have only one class of stock. Additionally, the shareholders must be individuals (that is, not another corporate entity). An S-Corp cannot have more than 100 shareholders (with family members eligible for treatment as a single shareholder). To qualify as an S-Corp for federal tax purposes the company must make an S-Corporation election through IRS Form 2553.

In order to form a S-Corporation the Articles of Organization must be filed. The Articles of Organization require basic information about the company such as the proposed name, registered agent name and address, and business purpose.

CorpCo® takes care of the preparation and filing of this document and can provide registered agent services in all 50 US States (and the District of Columbia). In addition, we can provide a variety of other services. For example, you may include Good standing, certified copy, or EIN (tax ID) obtainment services with your order.

Ready to form your S-Corporation?

Frequently Asked Questions

What happens when I order an S-Corporation formation from CorpCo?

You will receive confirmation of your order by email. At the same time, CorpCo will receive and review your request for accuracy and will begin preparing the necessary paperwork. CorpCo will draft your formation document and act as the organizer. The filing is then submitted to the state for processing. If your order includes Express Processing, it will take priority over other routine requests which means a faster processing time. While turnaround times vary greatly from state to state, routine processing is generally about 7-10 days. With CorpCo’s Express Processing, orders can be completed in as little as 24-48 hours in many states. Once your company has been approved by the state, CorpCo will send confirmation of filing which usually includes a file-stamped copy of the filing and an instrument of organization. If your company formation package includes a corporate kit, CorpCo will ship the kit under separate cover within 3-5 days of company formation.

The incorporation process is the same as the process to form a C-Corporation. In other words, the filings with the state do not look different for a C- Corporation or an S-Corporation. The difference in the two corporation types takes place with the federal (IRS) or state revenue division filings.

What is Form 2553 and how do I file it?

The 2553 is the IRS tax status election form which is required if a corporation wishes to be treated as an S-Corporation for tax purposes. This form must be filed within 75 days of the date of formation (or start of business), within 75 days of a new tax year, or any time during the year before the year the election should be effective.

What are the main differences between a C-Corporation and an S-Corporation?

C-Corporations file IRS form 1120 to report corporate income to the Internal Revenue Service. The IRS taxes company profits at corporate tax rates and dividends paid to shareholders at individual tax rates. For this reason, you may hear tax professionals refer to “double taxation” of a C-Corporation.

C-Corporations can elect “pass-through” taxation by applying to the IRS for status as a Subchapter S-Corporation (IRS form 2553). The S-Corporation provides the same protection from personal liability. However, owners can report their share of profit and loss in the company on their individual tax returns. The S-Corporation files IRS form 1120S to report income.

S Corporations have a number of restrictions. Most notably, only U.S. citizens or permanent residents may own an S-Corporation. An S-Corporation may not have more than 100 shareholders.

What is required to form an S-Corp?

In order to form an S-Corporation, Articles of Incorporation (sometimes referred to as a Certificate of Incorporation) must be filed with the state where the S- Corporation is to be formed. The Articles of Incorporation will require basic information about the company such as the proposed name, registered agent name and address, principal office address, and business purpose. CorpCo takes care of the preparation and filing of this document and can provide registered agent services in all 50 US States as well as the District of Columbia.

At the level of taxation, S-Status is not automatically assumed. It will be necessary to elect to be treated this way with the federal government by filing a form 2553 with the IRS. In addition to this special requirement with the IRS, the company may also be required to elect to be treated as an S-Corporation on the state level by filing a special form with that state’s revenue department.

What is required to keep my company active?

Each state has varying requirements for keeping the company active/in good standing. Most will require some sort of annual filing which may require company details and usually involve a filing fee. In some states, failure to file an annual tax return may also result in the company becoming inactive (not in good standing).